As individuals approach retirement in Florida, one of the most daunting challenges they face is projecting future investment returns to ensure their savings will last throughout their golden years. This article explores the difficulties in making such projections, examines recent market performance against predictions, and discusses various modeling approaches, ultimately advocating for a flexible, dynamic withdrawal strategy.

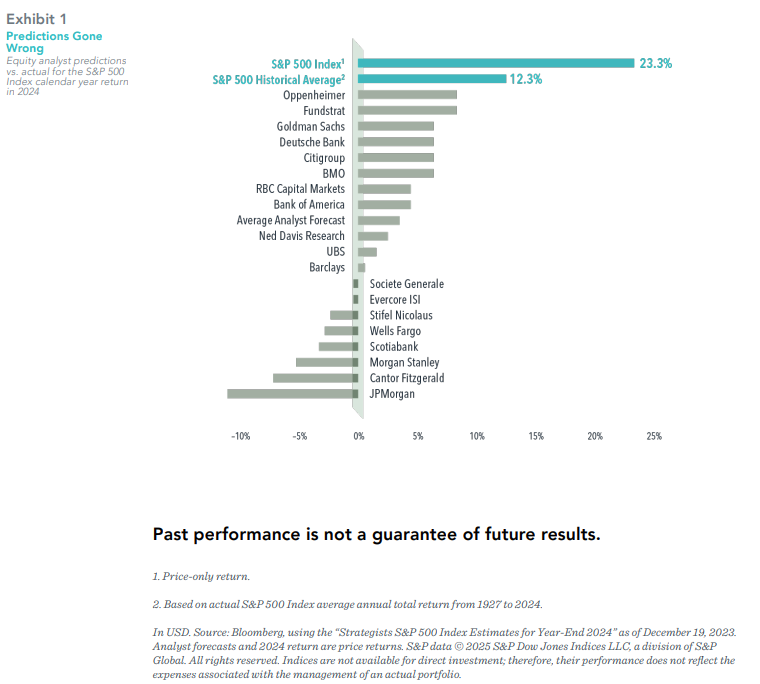

To illustrate the difficulty of predicting market returns, let's compare some notable forecasts for 2024 with the actual performance of S&P 500 Forecasts for 2024:

As we enter 2025, various financial institutions have released their long-term capital market assumptions for the US Markets:

The wide range of forecasts, particularly for the S&P 500, underscores the uncertainty inherent in market predictions.

Straight Line Modeling:

Traditional Monte Carlo Simulation:

Reduced-CMA Monte Carlo:

Historical Backtesting:

Regime-Based Monte Carlo:

When incorporating estimated returns into retirement plans, it's crucial to understand the strengths and limitations of various modeling approaches. A study on Kitces.com by Derek Tharp, PH.D, CFP, CLU, RICP, and Justin Fitzpatrick Ph.D, CFP, CFA provides valuable insights into the accuracy of different Monte Carlo methodologies. The study cites the best-performing Monte Carlo approaches were the Historical and Regime-Based Monte Carlo models. These methods significantly outperformed the more commonly used Traditional Monte Carlo and Reduced-CMA Monte Carlo approaches. Here are the key points about the best approaches:

Regime-Based Monte Carlo Observation:

Historical Monte Carlo Observation:

Both of these approaches were found to be more accurate and reliable than the Traditional Monte Carlo method, which is currently more commonly used in financial planning for retirement. The Regime-Based and Historical models seemed to capture real-world dynamics better, such as market momentum and mean reversion. It's important to note that while these approaches performed better, they still had significant levels of error. No Monte Carlo method was perfect, highlighting the need for ongoing monitoring and adjustments in retirement planning.

Given the challenges in accurately predicting returns, at Southshore Financial Planning we advocate for embracing unpredictability and adopting dynamic withdrawal strategies like the risk-based guardrail approach.

Here are the key points of this method:

While this approach requires more active management than traditional methods, it offers Florida retirees greater flexibility to adapt to personal circumstances and market conditions. It's like having a financial GPS that recalculates your route as conditions change, ensuring you stay on course towards your retirement goals.

The challenges of projecting future investment returns are numerous and complex. Historical data shows that even expert predictions can be wildly inaccurate, and various modeling approaches have their strengths and limitations. Given these uncertainties, retirees should consider working with financial planning firms that embrace flexible, dynamic withdrawal strategies like the Guardrails method. This allows individuals to better navigate the inevitable ups and downs of their investment portfolios. This approach, combined with regular plan reviews and adjustments, offers a more resilient path to financial security in retirement.

Southshore Financial Planning LLC is a registered investment adviser offering services in the State of Florida and in other jurisdictions where exempted. Registration does not imply a certain level of skill or training. This publication is for informational purposes only and is not intended as tax, accounting or legal advice, as an offer or solicitation of an offer to buy or sell, or as an endorsement of any company, security, fund, or other securities or non-securities offering. This publication should not be relied upon as the sole factor in an investment making decision. Past performance is no indication of future results. Investment in securities involves significant risk and has the potential for partial or complete loss of funds invested. It should not be assumed that any recommendations made by the Author, in the future, will be profitable or equal the performance noted in this publication. All opinions and estimates constitute Southshore Financial Planning LLC’s judgment as of the date the information was printed and are subject to change without notice. Southshore Financial Planning LLC does not warrant that the information will be free from error. The information should not be relied upon for purposes of transacting securities or other investments. Your use of the information is at your sole risk. Under no circumstances shall Southshore Financial Planning LLC be liable for any direct, indirect, special or consequential damages that result from the use of, or the inability to use, the information provided herein, even if Southshore Financial Planning LLC or a Southshore Financial Planning LLC authorized representative has been advised of the possibility of such damages. The information herein is provided “AS IS” and without warranties of any kind either express or implied. To the fullest extent permissible pursuant to applicable laws, Southshore Financial Planning LLC (referred to as “Southshore Financial Planning”) disclaims all warranties, express or implied, including, but not limited to, implied warranties of merchantability, non-infringement, and suitability for a particular purpose. Federal tax advice disclaimer: As required by U.S. Treasury Regulations, you are informed that, to the extent this presentation includes any federal tax advice, the presentation is not written by Southshore Financial Planning LLC to be used, and cannot be used, for the purpose of avoiding federal tax penalties. Use of any information presented by Southshore Financial Planning LLC is for general information only and does not represent individualized tax advice, either express or implied. You are encouraged to seek professional tax advice for income tax questions and assistance.

Chris Shoup, CFP®

Founder, Financial Advisor

We deliver financial planning and investment management strategies that are personalized to your needs, goals and lifestyle.

Talk with an AdvisorOffice: 1600 E 8th Ave., Ste. A200 Tampa, FL 33605

Additional Meeting Location: 200 Central Ave. St. Petersburg, FL 33701

© Southshore Financial Planning. All Rights Reserved. Privacy Policy. Form ADV. Designed by Converting Attention.

Southshore Financial Planning LLC (“Southshore Financial Planning”, “Southshore”) is a registered investment advisor offering advisory services in the State of Florida and in other jurisdictions where exempted. Registration does not imply a certain level of skill or training. The presence of this website on the Internet shall not be directly or indirectly interpreted as a solicitation of investment advisory services to persons of another jurisdiction unless otherwise permitted by statute. Follow-up or individualized responses to consumers in a particular state by Southshore Financial in the rendering of personalized investment advice for compensation shall not be made without our first complying with jurisdiction requirements or pursuant to an applicable state exemption.

All written content on this site is for information purposes only. Opinions expressed herein are solely those of Southshore Financial Planning, unless otherwise specifically cited. Material presented is believed to be from reliable sources, and no representations are made by our firm as to other parties’ informational accuracy or completeness. All information or ideas provided should be discussed in detail with an advisor, accountant or legal counsel prior to implementation.